Disclaimer: computer geeks like me are … well, maybe not the last people you want to consult on economic issues, but we're pretty far down the list. Nevertheless, let's see if we can contribute anything useful in the current brouhaha about the "Enron Loophole".

If you don't know what the Enron Loophole is, Google is your friend, at least in the sense it will lead you to a lot of people talking about it. For example (as I type), there's a news story headlined "Obama calls for 'Enron Loophole' to be closed"

Obama made the proposal just as his chief spokesman blasted former Texas Sen. Phil Gramm, a close friend and campaign adviser to Republican presidential contender John McCain, who Democrats say created the loophole in 2000.

Ah, it's beginning to make a little sense. A WSJ blog notes:

There are a lot of warning flags here. First, partisan points are

scored, always a signal that the truth is almost certainly not

the driving force behind this.

In addition,

we note the obvious scapegoating of

"speculators," a relatively tiny number of easily-demonized

investors

who perform a function that only a minuscule fraction of the citizenry

understand.

It's great political

theater: Congress gets to "do something" about

oil prices, hopefully impressing the rubes voters

without actually making any tough decisions that would

directly impact large numbers of people.

Also note Corzine's comment about "too much speculation". Sure. Governor Corzine knows what the "right" amount of speculation is, and that regulatory legislation will get it exactly right. And if you believe that, I have approximately 932 e-mail messages from Nigeria that will make you a fantastically wealthy person.

And finally, the term "Enron loophole" is Lakoff-style "framing": setting the terms of the debate by rhetorical capture of an ad-worthy term. Nobody likes "loopholes"; everybody knows we're supposed to despise Enron. (And I guess we're not supposed to ask, despite having that loophole going for them, how they nevertheless crashed and burned.)

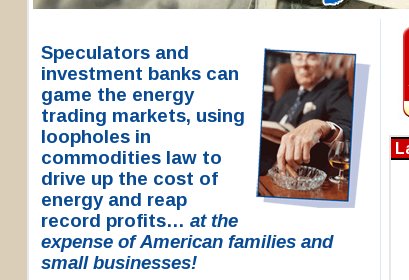

Onward: also high on the Google hit list is www.closetheenronloophole.com, a website set up to advocate government action to, well, close the Enron loophole. The site reeks of demagogic populism:

Families and small businesses! Victimized by that fancy-dressin' coldly aloof guy with the cigar! The site is hardly reticent:

Yes, that's an all-uppercase dirty-word PROFIT. Who are the brave profit-disparaging folks behind this website? Aaaallll the way down at the bottom of the page:

The Petroleum Marketers Association of America. They have a their website here.

Hmmm. On the face of it, not exactly a bunch of grassroots citizens rising up in righteous anger. But they also have "Platinum Partners":

- Altria Corporate Services/Philip Morris, U. S. A.

- BP Products North America, Inc.

- CITGO Petroleum Corporation

- Chevron Products Company

- ConocoPhillips

- ExxonMobil

- Federated Insurance Company

- National Biodiesel Board

- R. J. Reynolds

- Shell Oil Products US

- UST, Inc

- Valero Marketing and Supply Company

Ah, yes. The normal coalition of left-wing socialist wackos who treat PROFIT as a dirty word.

My BS detector is beeping like mad. But there's one more test. Does Paul Krugman join in the partisan scapegoating? Let's check his NYT blog. Here's a gem:

The short answer is that I think his testimony is just stupid.

As a second data point, note that another reliable Democratic partisan, Brad DeLong, simply quotes Krugman on this issue without quibbling.

DeLong and Krugman are the dogs that don't bark on this issue. If they could join in the GOP-bashing chorus about oil speculation, they'd do it. As near as I can tell, they're not. What does that tell you?

![[The Blogger and His Dog]](/ps/images/me_with_barney.jpg)